One of the most common questions we hear from prospective buyers is:

"Should we wait to buy until mortgage rates come down?"

It's a reasonable question. After all, even a small change in interest rates can affect your monthly payment.

But here's the challenge: focusing only on mortgage rates can cause buyers to overlook several other factors that may have just as much—or even more—impact on the total cost of buying a home.

The truth is, there isn't a universally "right" time to buy. Every situation is different. However, understanding the trade-offs can help you make a more informed decision instead of waiting simply because you're hoping the market changes.

Mortgage Rates Are Only One Piece of the Puzzle

Everyone hopes mortgage rates will decline.

They might.

They also might not.

Even professional economists and financial markets have difficulty predicting where rates will be six months from now. While rates have moved lower from their recent highs, no one can say with certainty what they'll do next.

More importantly, mortgage rates aren't the only factor that determines affordability.

The purchase price, property taxes, insurance costs, loan terms, and any seller concessions all play a role in what you'll actually pay each month.

Related Reading: The Fed Just Met. What Does That Mean for Mortgage Rates? (June 18, 2026)

👉 https://www.findwacohomes.com/blog/fed-just-met-what-does-mean-mortgage-rates/

Home Prices Don't Always Move the Way People Expect

Some buyers assume that waiting will automatically result in lower home prices.

Sometimes that's true.

Sometimes it isn't.

Even in today's more balanced market, well-priced homes in desirable neighborhoods continue to sell quickly. If demand increases or inventory tightens, prices can stabilize—or even rise—before mortgage rates change significantly.

Trying to perfectly time the housing market is incredibly difficult.

For most families, buying when they're financially ready is often a better strategy than trying to predict what the market will do next.

Today's Incentives May Not Be Around Forever

One advantage buyers have in today's market is negotiating power.

Depending on the property, buyers may be able to negotiate:

- Closing cost assistance

- Interest rate buydowns

- Builder incentives

- Repair allowances

- Flexible closing dates

Those opportunities tend to become less common when buyer demand increases.

If the market becomes more competitive in the future, many of these incentives could disappear.

That's worth considering when deciding whether waiting will actually save money.

Rent Is Still a Housing Expense

If you're currently renting, waiting has a cost too.

Every month of rent is another month you're paying for housing without building equity.

That doesn't automatically make buying the better decision. Renting can absolutely be the right choice depending on your goals and financial situation.

The important thing is recognizing that waiting isn't free.

It's another piece of the financial equation.

Life Doesn't Always Follow the Housing Market

Many people don't move because the market tells them to.

They move because life changes.

Perhaps your family is growing.

Maybe you've accepted a new job.

You might want to be closer to family, shorten your commute, or move into a neighborhood with different schools.

Those personal factors often matter more than whether mortgage rates are a quarter-point higher or lower.

Buying a home should support your life—not the other way around.

A Local Perspective

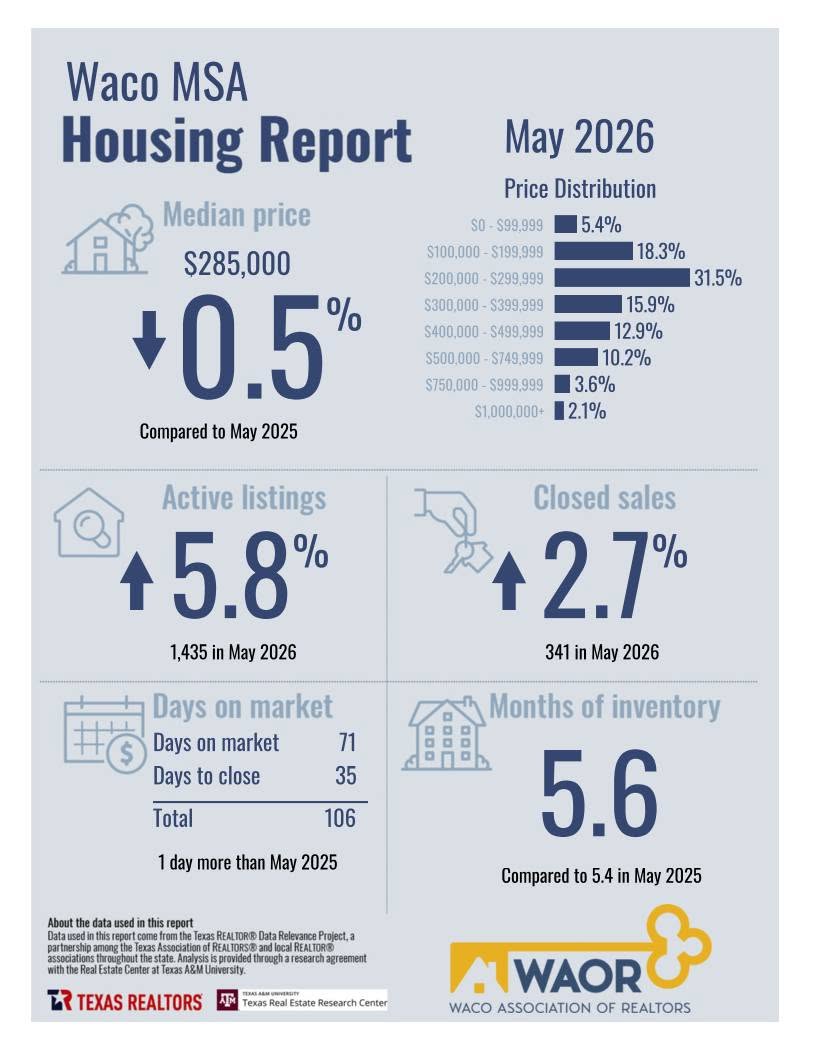

Here in the Waco area, we're seeing a housing market that's become much more balanced than it was a few years ago.

Buyers generally have more homes to choose from, more time to make decisions, and in many cases, greater opportunities to negotiate than they did during the highly competitive market of 2021 and 2022.

That doesn't mean every buyer should rush into purchasing a home.

It simply means that waiting isn't automatically the safer—or less expensive—option many people assume.

The best time to buy is when you're financially prepared, your goals are clear, and the right home comes along.

Final Thoughts

No one has a crystal ball.

Mortgage rates may fall.

Home prices may change.

New opportunities may appear.

Or they may not.

Rather than trying to perfectly predict the market, focus on the factors you can control: your finances, your long-term plans, and finding a home that fits your needs.

If you're wondering whether now is the right time to buy—or whether waiting makes more sense—we'd be happy to help you evaluate your options based on your specific situation, not just the latest headlines.

Related Articles

The Fed Just Met. What Does That Mean for Mortgage Rates? (June 18, 2026)

👉 https://www.findwacohomes.com/blog/fed-just-met-what-does-mean-mortgage-rates/

The Real Cost of Buying a Home in Waco (Beyond the Down Payment) (February 24, 2026)

👉 https://www.findwacohomes.com/blog/real-cost-of-buying-a-home-in-waco/

Should You Buy Your Next Home Before Selling Your Current One? (July 7, 2026)

👉 https://www.findwacohomes.com/blog/should-you-buy-your-next-home-selling-your-current-one/

.png)

.png)